A new era of education benefits.

You need modern strategies to support your workforce.

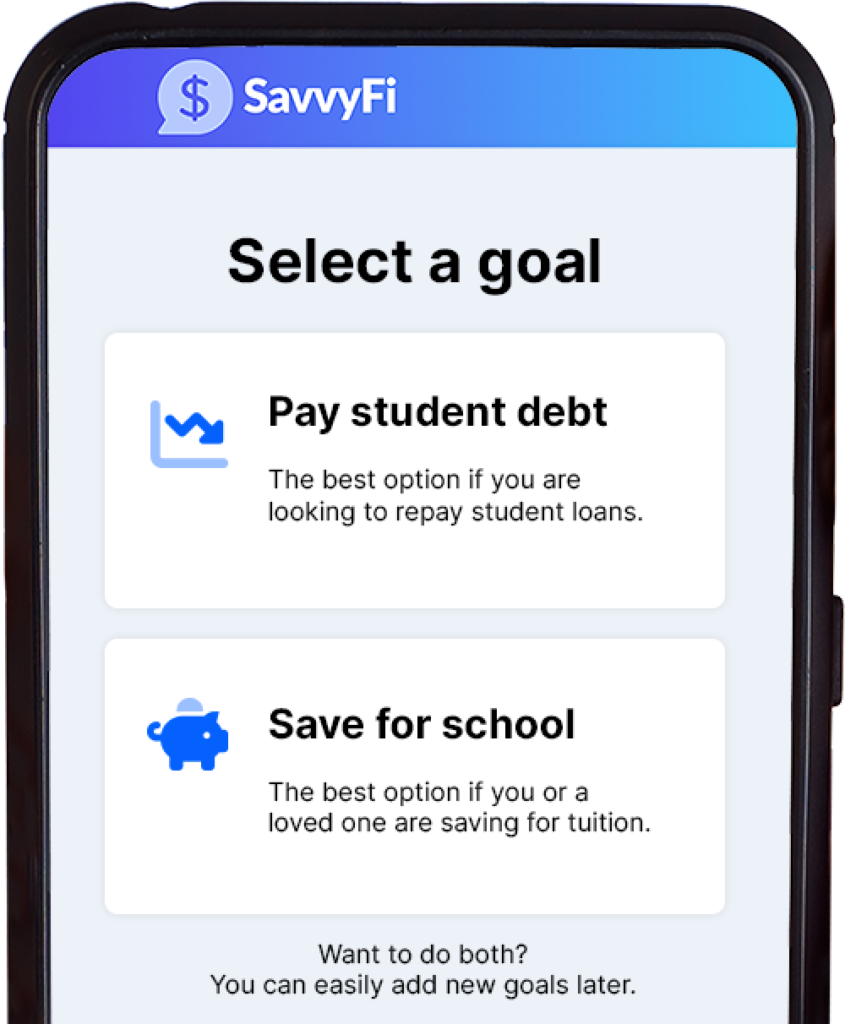

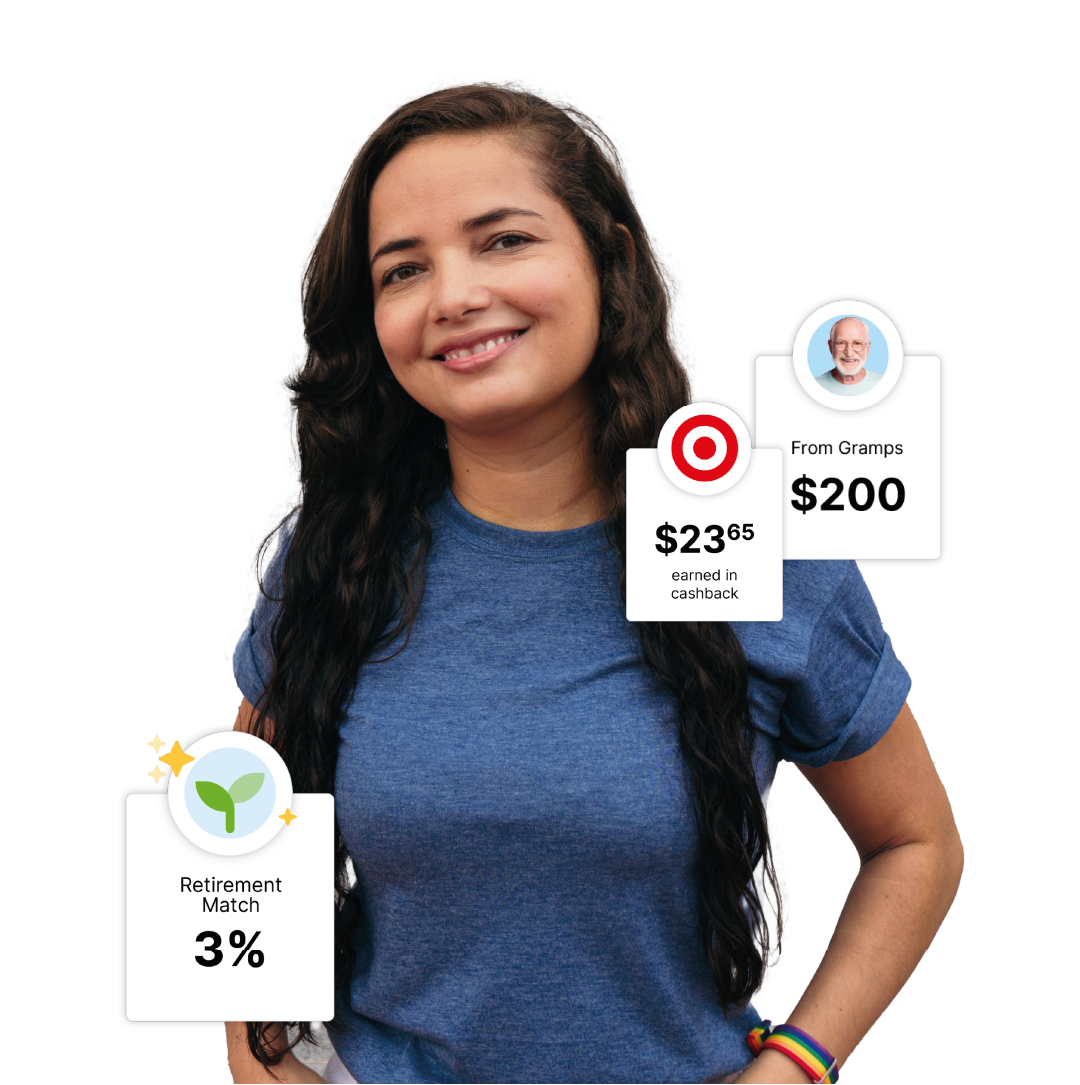

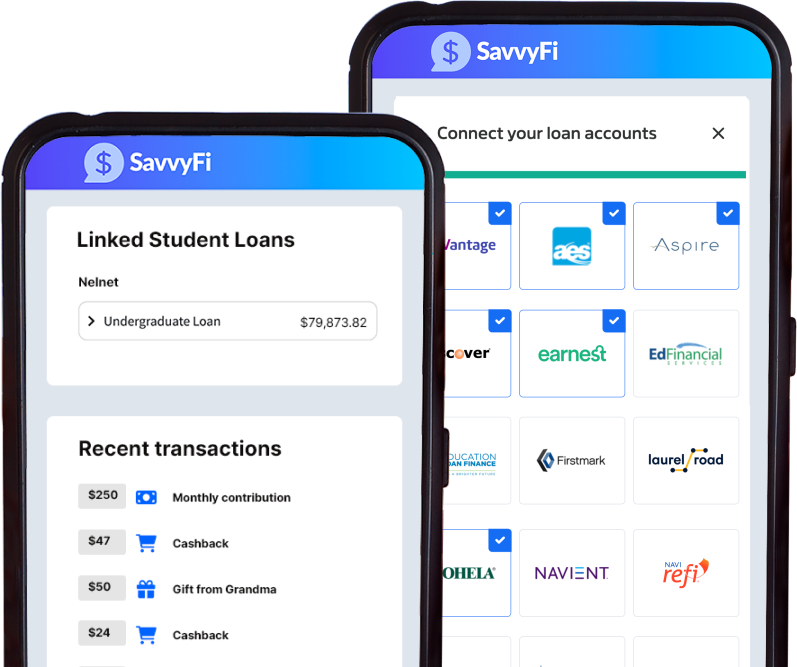

We help you offer a range of education financial benefits — from tackling existing student loan debt to investing for the future.

Let’s make a real impact on your employees’ financial futures.

![]()

SOC-2 Compliant

SOC-2 Compliant